1. Global equity markets rebounded in May after a weak April.

This chart shows the performance of SPY (SPDR S&P 500 Index ETF in purple), EFA (iShares MSCI EAFE ETF in blue), EEM (iShares MSCI Emerging Markets ETF in orange), and IWM (iShares Russell 2000 ETF in grey).

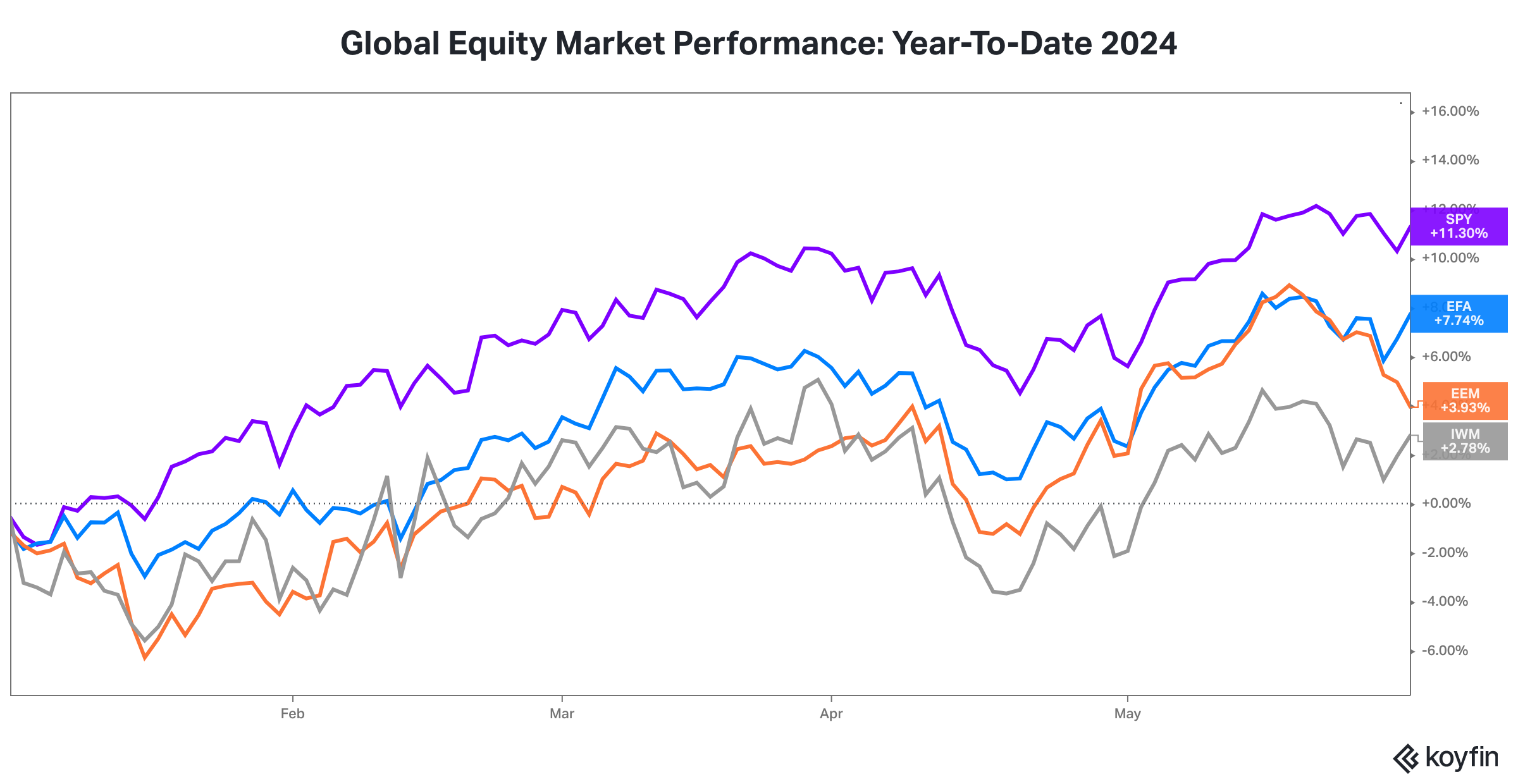

2. Equity investors have enjoyed strong returns year-to-date.

This chart shows the performance of SPY (SPDR S&P 500 Index ETF in purple), EFA (iShares MSCI EAFE ETF in blue), EEM (iShares MSCI Emerging Markets ETF in orange), and IWM (iShares Russell 2000 ETF in grey).

3. Bond investors haven’t fared as well due to the increase in interest rates at intermediate and long maturities.

Source: www.treasury.gov, Two Centuries Investments

4. Sticky inflation, in the face of high public debt and high fiscal deficits in the developed world, remains a big headwind for investors seeking high real returns (real return = nominal return - rate of inflation).

In the U.S., the headline inflation rate has plateaued over 1% above pre-pandemic levels.

The “core” inflation rate (excludes food and energy) has continued to creep down but also remains over 1% above pre-pandemic levels.

Due to sticky inflation, the FOMC has kept the effective federal funds rate at 5.33% for the past year.

We discussed the inflation challenge in more detail in April’s market update.

5. Despite sticky inflation and no rate cuts by the FOMC, U.S. financial conditions remain loose and U.S. credit markets remain sanguine.

Over the last few months, the Chicago Fed’s National Financial Conditions Index has been signaling looser financial conditions, suggesting monetary policy is not restrictive despite 525 basis points of federal funds rate increases over the last two years.

At month end May 2024. high yield bond spreads remained subdued and had settled almost 200 basis points below the long-term average and well below recent peaks.