“Are we there yet?” is a refrain we hear frequently. “There” is the end of the sell-off in stocks and other asset classes.

If the Federal Reserve keeps tightening monetary policy to lower inflation, then we are not “there” yet.

As we explained last month, we believe inflation will continue to decline. We are uncertain about the pace of decline and at what level inflation will settle, mostly because underinvestment in exploration and production will likely mean high crude oil and natural gas prices for an extended period.

The sooner inflation approaches ~4%, the more likely the Federal Reserve stops raising the Federal Funds Rate, and the more likely the US can avoid both a sharp decline in economic activity and a credit crisis. Once the worst case scenario is off the table, the equity market will likely have found its bottom.

1. In September, all major asset classes sold off. Risky assets, namely stocks and corporate credit, sold off. Flight to quality assets, namely US Treasuries and gold, also sold off.

This chart shows the price performance of IAU (iShares Gold Trust in yellow), JNK (SPDR Bloomberg High Yield Bond ETF in gray), LQD (iShares iBoxx $ Investment Grade Corporate Bond ETF), TLT (iShares 20+ Year Treasury Bond ETF in red), EFA (iShares MSCI EAFE ETF in purple), SPY (SPDR S&P 500 Index ETF in blue), and EEM (iShares MSCI Emerging Markets ETF in orange).

2. In August, U.S. inflation rate (as measured by CPI-U) fell to a 8.3% from July’s 8.5% and June’s 9.0% rate, which was the highest annual rate since the 1970s.

We anticipate inflation in the U.S. to moderate as the demand for goods continues to ease post pandemic. However, labor market challenges, structurally higher energy prices, and supply chain challenges emanating from China will put a floor on the intermediate term range for inflation.

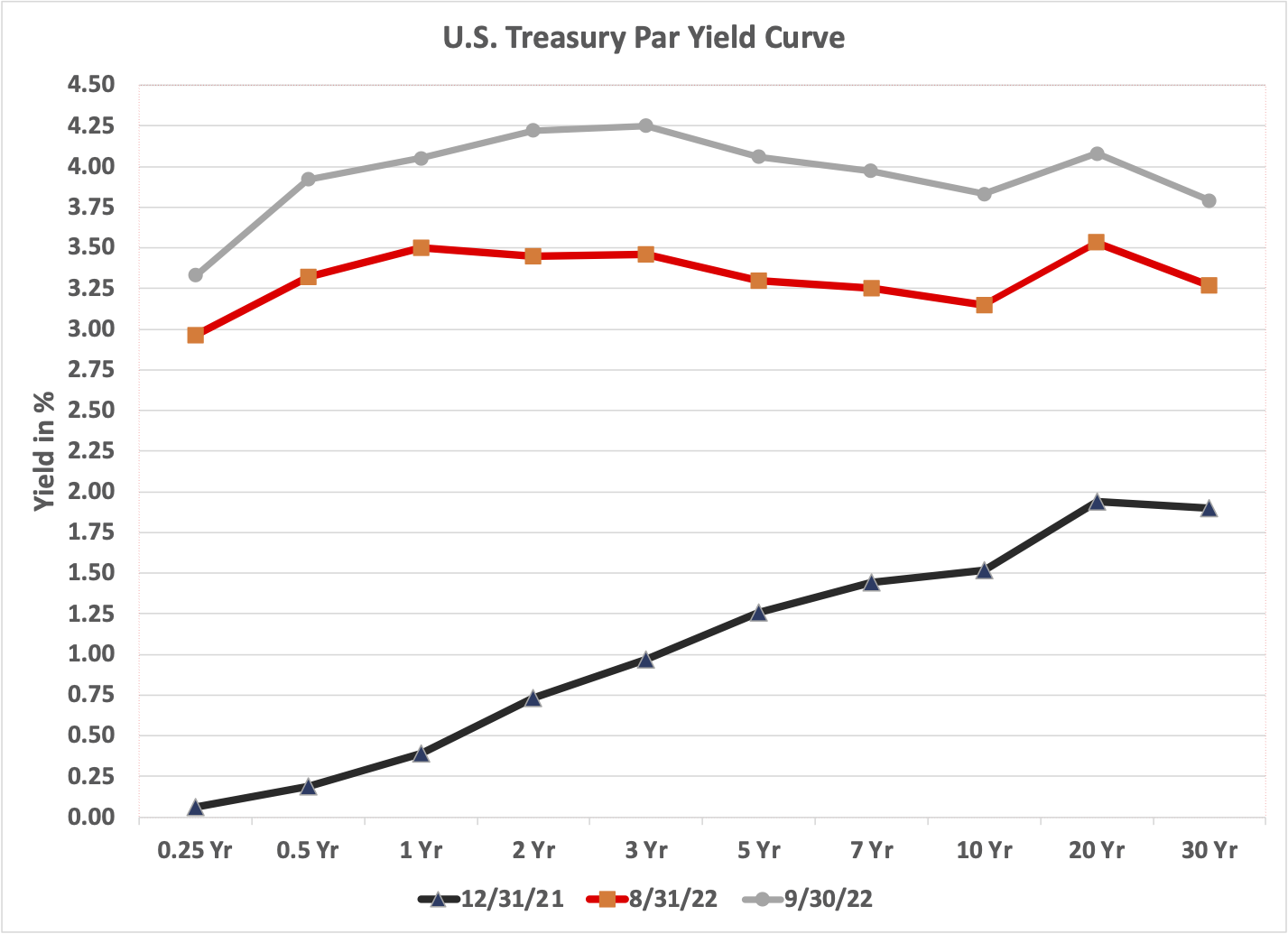

3. US interest rates continued their rise, wreaking havoc on all major asset classes, as the Federal Reserve raised the Federal Funds Rate by 0.75% in September. The Fed has raised the rate by 2.75% so far in 2022.

Source: treasury.gov, Two Centuries Investments

4. The good news is credit risk remains subdued. Yes, credit spreads are off their recent lows at the end of 2021 and beginning of 2022. However, spreads are well below the 2020 pandemic peak and even well below the 2016 peak. Credit conditions bear monitoring for signs of stress.

5. The strength of the US dollar also bears monitoring. Continued strengthening will be more than sand in the gears of global economic activity. It threatens to be a wrecking ball.

This chart shows the performance of the DXY Index, an index (or measure) of the value of the United States dollar relative to a basket of foreign currencies.

The US dollar is the world’s reserve currency. Approximately 40% of global trade is invoiced in US dollars. Most commodities are priced in US dollars, most importantly crude oil. Many nations and many non-US companies have some debt denominated in US dollars. When the US dollar rises, it represents an increase in expenses for many non-US entities.